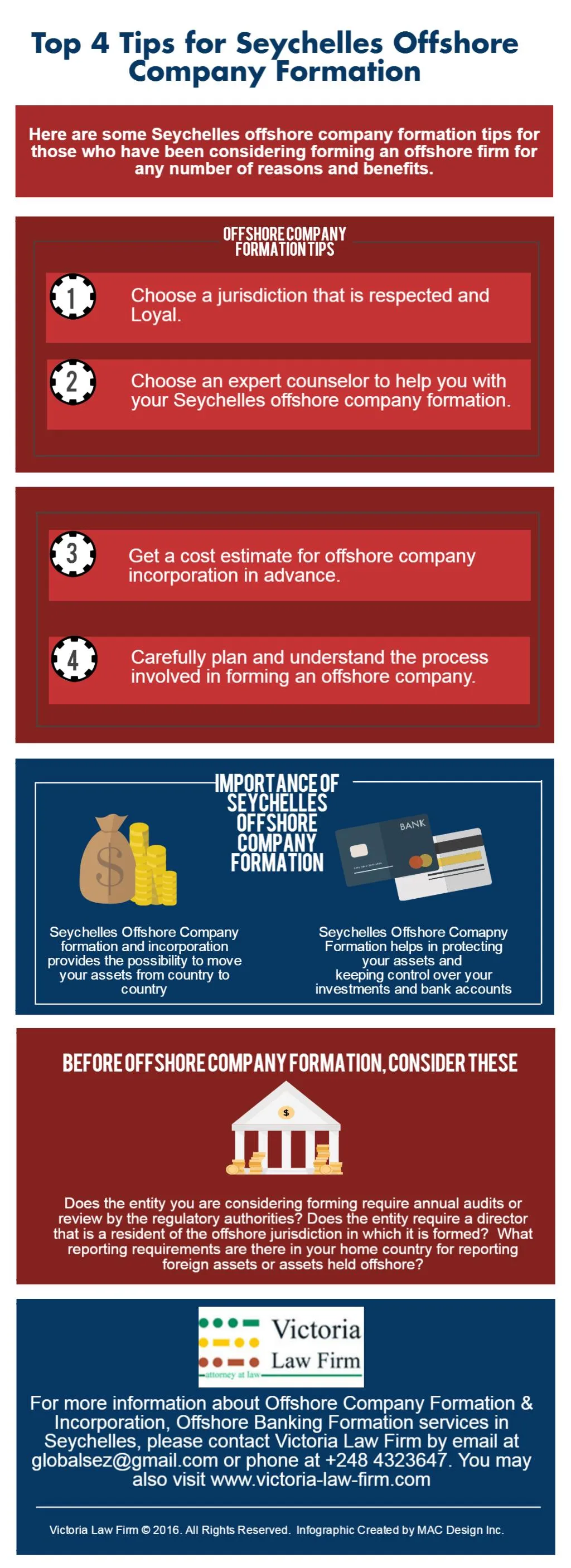

Recognizing Offshore Company Formations: A Comprehensive Overview to the Process and Advantages

Offshore business formations provide a strategic opportunity for entrepreneurs looking for to enhance their business procedures. These entities usually offer advantages such as tax advantages, increased privacy, and robust property defense. Understanding the complexities of selecting a territory, the formation process, and conformity needs is important. As the landscape of international company advances, the effects of establishing an offshore company warrant careful consideration. What steps should one require to navigate this facility surface?

What Is an Offshore Firm?

An offshore company is an organization entity incorporated outside the jurisdiction of its owners' house, often in a country with positive regulative and tax atmospheres. These companies can serve different functions, including possession protection, worldwide trading, and riches administration. They are typically developed in jurisdictions understood as tax havens, where company tax rates are low or missing, and privacy legislations are stringent.

Offshore business may be had by people or other business entities and can run in different markets, including e-commerce, consulting, and finance. While they provide particular advantages, the lawful and regulative structures governing overseas companies vary considerably by territory. Organization proprietors should navigate these intricacies to assure conformity with both regional and worldwide regulations. Comprehending the structure and function of offshore companies is crucial for individuals considering this option for business operations or possession management.

Benefits of Developing an Offshore Company

While the decision to develop an offshore company may stem from various tactical considerations, the potential benefits are engaging for many company owner. One considerable benefit is tax optimization; numerous offshore jurisdictions offer positive tax obligation prices or perhaps tax exemptions, allowing firms to maintain more revenues. In addition, overseas companies usually supply improved personal privacy protection, protecting the identities of shareholders and supervisors from public analysis.

Finally, local business owner may discover operational flexibility, as offshore territories regularly have fewer governing hurdles, allowing streamlined administration and administration. Jointly, these advantages make overseas company formations an appealing choice for many looking for to expand their business perspectives.

Picking the Right Jurisdiction

Selecting the proper jurisdiction for an offshore business is an important action in making best use of the advantages outlined earlier. Different factors influence this choice, consisting of tax obligation laws, business legislations, and the total company atmosphere. Jurisdictions such as the British Virgin Islands, Cayman Islands, and Singapore are frequently favored for their favorable tax obligation regimes and durable legal frameworks.

It is necessary to take into account the certain requirements of the business, such as personal privacy needs and governing compliance. In addition, the convenience of working, including the effectiveness of firm enrollment and financial facilities, plays a considerable function.

Possible owners should likewise evaluate the political security and reputation of the picked territory, as these aspects can impact long-lasting success. Eventually, thorough research study and specialist appointment are recommended to ensure positioning with the firm's objectives and to leverage the full potential of offshore benefits.

The Offshore Firm Formation Refine

The overseas business development procedure includes a collection of crucial steps that call for cautious preparation and execution. At first, people or organizations need to choose an appropriate jurisdiction that straightens with their objectives, considering factors such as tax obligation benefits, personal privacy, and regulatory environment. Following this, the following step requires picking the proper service framework, such as an International Company Firm (IBC) or Limited Liability Company (LLC)

As soon as the framework is identified, needed records, consisting of a business strategy, recognition, and proof of address, must be prepared. Involving a credible neighborhood representative or company can improve this stage, making certain compliance with regional guidelines. After sending the called for documentation to the pertinent authorities, the formation process generally finishes in the issuance of a certificate of unification. This paper establishes the firm as a lawful entity, enabling it to conduct company globally.

Legal Needs and Compliance

Understanding the legal demands and conformity commitments is necessary for any person aiming to establish an overseas firm. Each jurisdiction has particular policies that need to be abided by, which can include company registration, obtaining essential licenses, and keeping neighborhood addresses. Offshore Company Formations. It is vital to select a registered agent that can promote communication with local authorities and warranty conformity with recurring coverage requirements

In addition, numerous territories need the submission of annual monetary statements, together with tax filings, also if the firm does not generate income. Directors and shareholders must be determined, with due persistance treatments usually mandated to validate their identities. Failing to satisfy these lawful obligations can lead to fines or the dissolution of the firm. Consequently, potential offshore company proprietors should talk to lawyers experienced in worldwide business legislation to browse these complexities properly and assure full compliance with all policies.

Tax Ramifications of Offshore Companies

The tax effects of offshore firms existing significant advantages that draw in several business owners. Understanding the linked compliance demands is necessary for navigating the complexities of worldwide tax legislations. This section will check out both the potential advantages and the essential responsibilities connected to overseas business structures.

Tax Advantages Introduction

Offshore firms are typically checked out with skepticism, they can use substantial tax benefits for companies and individuals looking for to optimize their economic approaches. Among the main benefits is the potential for lower business tax rates, which can bring about substantial financial savings. Numerous offshore jurisdictions supply desirable tax obligation regimens, consisting of absolutely no or marginal tax obligation on earnings, funding gains, and inheritance. In addition, overseas business can help with global organization operations by minimizing tax obligation obligations related to cross-border deals. This framework might also enable tax obligation deferral possibilities, enabling revenues to grow without prompt taxes. Eventually, these benefits add to improved monetary efficiency and asset protection, making overseas business an appealing option for smart financiers and entrepreneurs.

Compliance Requirements Described

Offshore business might present tax advantages, but they likewise include a set of compliance demands that need to be thoroughly navigated. These entities go through details reporting responsibilities, which differ substantially depending on the jurisdiction. Normally, offshore business need to preserve exact economic documents and submit annual economic statements to adhere to regional guidelines. In addition, numerous territories call for the disclosure of useful ownership to battle money laundering and tax obligation evasion. Failing to follow these compliance procedures can result in serious charges, including fines and prospective loss of service licenses. Recognizing the regional tax obligation regulations and international contracts is vital, as they can influence tax responsibilities and total operational validity. Engaging with economic and legal specialists is a good idea to ensure full conformity.

Preserving and Handling Your Offshore Company

Preserving and taking care of an overseas business includes sticking to various continuous compliance demands vital for lawful operation. This includes diligent economic document keeping and an understanding of tax obligation commitments pertinent to the business's territory. Effective monitoring not just ensures this post regulative compliance but additionally sustains the firm's financial health and wellness and longevity.

Continuous Compliance Needs

Assuring ongoing compliance is important for any entity operating in the overseas field, as failing to meet regulatory demands can cause significant charges and even dissolution of the company. Offshore firms need to abide by neighborhood regulations, which may consist of annual filing of financial statements, payment of essential costs, and preserving a registered office address. Furthermore, business are typically required to assign a local agent or representative to assist in communication with authorities. Routine updates on adjustments in regulations or tax demands are essential for conformity. Adherence to anti-money laundering (AML) and know-your-customer (KYC) policies is important. By preserving organized documents and remaining informed, overseas business can guarantee they continue to be compliant and alleviate threats related to non-compliance.

Financial Document Maintaining

Efficient economic record maintaining is vital for the effective management of any kind of overseas firm. Preserving precise and detailed monetary documents help in tracking the business's performance, assuring conformity with regional policies, and promoting notified decision-making. Companies ought to carry out methodical processes for recording revenue, expenses, and transactions to create openness and responsibility. Making use of accounting software program can enhance this process, enabling real-time economic evaluation and coverage. Consistently assessing economic statements assists identify fads, analyze profitability, and handle money flow efficiently. Additionally, it is vital to firmly keep these records to safeguard delicate details and assurance easy accessibility throughout audits or financial testimonials. By prioritizing thorough monetary record keeping, offshore companies can improve operational performance and support long-term success.

Tax Obligations Overview

Recognizing tax responsibilities is vital for the appropriate management of an overseas company, as it directly influences economic performance and conformity. Offshore companies might undergo numerous tax obligation legislations depending upon their jurisdiction, consisting of business tax obligations, value-added tax obligations, and withholding taxes. It is imperative for entrepreneur to remain informed regarding their tax obligation responsibilities, as failure to comply can lead to charges and legal concerns. In addition, numerous overseas jurisdictions offer tax obligation motivations, which can greatly benefit businesses if navigated correctly. Involving a well-informed tax expert or accounting professional focusing on worldwide tax obligation regulation can assist ensure that firms meet their obligations while enhancing their tax obligation techniques. Inevitably, persistent tax obligation management contributes to the overall success and sustainability of an overseas entity.

Regularly Asked Inquiries

Can I Open a Bank Account for My Offshore Company From Another Location?

The ability to open up a financial institution account for an offshore firm from another location relies on the financial institution's policies and the territory's policies. Many financial institutions supply remote solutions, however specific requirements may vary significantly between institutions.

What Are the Costs Associated With Forming an Offshore Company?

The costs associated with forming an offshore company commonly include registration fees, lawful and consulting expenditures, and continuous upkeep costs. These costs vary considerably based upon jurisdiction, intricacy of the organization structure, and specific solutions required.

Are There Limitations on Who Can Be a Shareholder?

Restrictions on shareholders differ by jurisdiction. Some countries might enforce constraints based on race, organization, or residency kind - Offshore Company Formations. It's crucial for possible financiers to research study certain policies suitable to their picked offshore location

Exactly how Lengthy Does the Offshore Company Development Refine Typically Take?

The overseas firm formation process generally takes between a couple of days to several weeks. weblink Aspects affecting the timeline consist of jurisdiction needs, document prep work, and responsiveness of pertinent authorities associated with the enrollment procedure.

What Occurs if I Fail to Abide By Neighborhood Regulations?

Failing to abide by local legislations can cause serious fines, including fines, lawful activity, or loss of service licenses - Offshore Company Formations. It may additionally damage the firm's reputation and prevent future organization chances in the territory

An offshore firm is a business you can check here entity included outside the territory of its owners' home, often in a country with desirable regulatory and tax obligation environments. One significant benefit is tax obligation optimization; numerous overseas jurisdictions offer beneficial tax obligation rates or also tax obligation exceptions, allowing companies to preserve even more profits. Offshore companies are usually watched with apprehension, they can offer significant tax advantages for companies and individuals seeking to optimize their monetary techniques. Furthermore, offshore business can facilitate global business operations by minimizing tax obligation responsibilities linked with cross-border transactions. Offshore firms may be subject to various tax laws depending on their jurisdiction, including corporate taxes, value-added taxes, and withholding taxes.